This post is an update of one I originally wrote in 2015 for University of Illinois Extension’s Plan Well, Retire Well blog.

Over the past couple of months, I have been talking with a young friend about a variety of financial topics. The challenges my young friend faces are the same things that almost all young adults deal with. Over the next few months, I’ll be sharing some of our conversations. Maybe you’re wrestling with some of the same questions. Or, like me, maybe you have a young friend you could share these conversations with. ~ Karen

Dear Karen,

You mentioned that putting my long-term savings into an IRA could save me some money on income taxes. How would that work? ~ Your Young Friend

Dear Young Friend,

If you put your money in a regular account, sometimes called a taxable account, such as one that you set up with a mutual fund company or a brokerage, you will owe taxes each year on any income in the account. That could be interest from a bonds, dividends from stocks, or any gain (profit) on stocks or bonds that were sold. You might also own these things indirectly, in a mutual fund that owns these things inside of it.

But if you tell the financial institution that you want to open a Roth IRA instead of a regular account, you won’t ever pay tax on the income in the account. (There are rules to qualify for that.) Being an IRA doesn’t change what investments you can have in the account, it just changes how the money is taxed.

If you told them to make it a traditional IRA instead of a Roth, you’d get income tax savings now instead of in the future. The money you put in a traditional IRA would be deducted from your income this year. You wouldn’t pay tax on that money – or on the growth in the account – until you took it out. That’s called tax deferral.

This won’t affect you right now, but just FYI – taxpayers who have a retirement plan at work and make more than a certain amount of money will not be able to deduct their contribution to a traditional IRA, or the deductible amount is limited. But you aren’t making enough money yet to worry about that. The deduction phases out for single filers with modified adjusted gross income between $77,000 and $87,000 and married filing jointly between $123,000 and $143,000 (2024).

Mathematically, those two tax breaks are equal if everything else stays the same. Which one is better depends on the situation. My guess is that the Roth would be a better choice for you. Here’s why:

You’re just starting your professional career, so your income is relatively low right now. That puts you in a low tax bracket, and the tax savings you’d get by deducting a contribution to a traditional IRA would be small. It’s likely that you’ll be in a higher tax bracket when you’re older. Being able to take money out of the Roth IRA then, without owing any tax on it, will be a much bigger advantage.

Tax rates can change. If they go up, you’ll be glad to have money you can take out tax-free.

A Roth IRA has one feature that is different from any other retirement account. You can take your contributions out any time, without any tax or penalty. All the other retirement accounts have penalties if you take money out before age 59 ½. With tax-deferred accounts, you’ll owe income tax plus a 10% penalty unless you qualify for an exception *******LINK*******. With a designated Roth account inside your employer retirement plan, you may not be able to access the funds at all until you retire or leave the company. And if you do take money out, it will be considered a mix of contributions and earnings. On the earnings portion, you’ll owe tax and an early distribution penalty.

Age 59 ½ is a long way off for you, and who knows what could happen between now and then? So the Roth IRA gives you a lot of flexibility that the other retirement plans don’t. If you really need the money, you can take out everything that you put in. At any time. No taxes. No penalties. If you take out more than the amount that you contributed, you’ll be dipping into the earnings or the growth in the account. If you take that money out and you aren’t yet age 59 ½, then you’ll owe income tax and a 10% penalty. But that doesn’t happen until you’ve taken out every penny that you contributed.

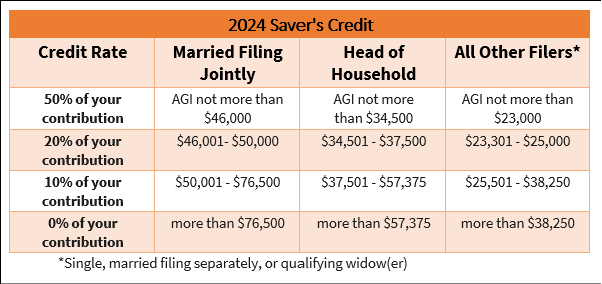

There’s another tax reason you should think about putting money into some type of retirement account, and that’s the Saver’s Credit. You can get this Credit no matter what kind of retirement plan you contribute to, as long as your income qualifies. The Credit is subtracted from your income tax. You can contribute up to $2000 and get a credit of 10%, 20% or 50% of that amount, depending on your income. (Married couples filing jointly could take the credit on up to $4000.) You have until the due date for filing your taxes – April 15 – to make the contribution and have it count for the prior year.

Here are the income limits for 2024. (Tables for 2023, 2022, and 2021)

Let’s say your Adjusted Gross Income is $27,000 and you’re single, so you look at the All Other Filers column. If you put $2000 into an IRA, your credit would be 10% of $2000 = $200. When you file your income taxes, you will get an extra $200 refund from the IRS. The only time you wouldn’t get the refund is if you didn’t owe any tax to start with.

If you’re eligible for the Saver’s Credit, it’s like someone is giving you a bonus. You contributed $2000, but it really only cost you $1800 to do it!

Karen

Copyright 2015, University of Illinois. Used with permission of University of Illinois Extension. Revised 2023 by Karen Chan, Karen Chan Financial Education & Consulting, LLC.

Leave a comment